Deflation is Always & Everywhere a Technological Phenomenon

Deflation is Always & Everywhere a Technological Phenomenon

#7 Look Up! Weekly

This title is inspired by a recent essay by Trevor Jackson for Foreign Policy, in which Jackson argues that Universal Basic Income (UBI) is a necessary tool to counter the massive deflationary spiral triggered by the global reaction to COVID19.

He writes,

“The danger of deflation means that the Fed’s gargantuan interventions may well save the financial system but not avert a grinding decade of unemployment, inequality, and instability — which is exactly what happened in 2008.”

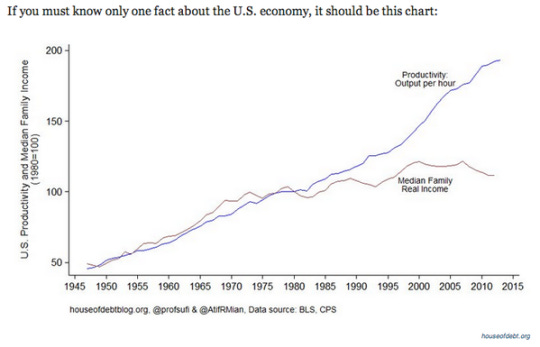

He uses the “quit rate” to illustrate his point. The “quit rate” is an indication of whether workers think they can leave their jobs for better ones. Although we have experienced consistent gains in GDP and reduced unemployment over the last 12 years since the Great Financial Crisis, the quite rate only recently reached pre-crisis levels. This illustrates that post-crisis gains mostly accrued to the top end of the income distribution.

That is where we were before COVID19.

Since the start of quarantine over 36 million Americans have lost their jobs. It is expected that tens of millions more have lost 2nd or 3rd income streams, received a pay cut, or are now less secure in their current position (as illustrated by a massive decline in the quit rate in March). When businesses that received government SBA and PPP support eventually spend these funds, all of these metrics will look far worse (even if lockdown has ended).

Yet, stock market returns over the last few months paint a different picture with the S&P increasing 32% since it bottomed at the end of March. Some argue that this is a result of Fed action, but it is also likely evidence that deflation is a technological phenomenon.

Why?

In February 2020, 5 big tech companies (FAAAM) accounted for +20% large of the S&P 500 index; COVID19 merely accelerated the wealth transfer to these behemoths.

COVID19 has accelerated the move to the cloud. While “main street” has suffered, tech has thrived. This is illustrated by the 42% increase in CLIX, an ETF that is 100% long e-commerce companies, and 50% short traditional retailers.

In an ironic twist, the deflationary effect of technology will start to negatively impact Big Tech employees themselves.

Last week, a wave of tech companies including Facebook, Shopify, and Coinbase declared themselves to be “remote-first,” — their employees are no longer required to travel to a physical office, but can instead work from home.

On the surface, this seems like a huge win for employees who are already fleeing San Francisco for cities with cheaper housing, lower taxes, and fewer homeless.

However, I’d be surprised if the move to “remote first” doesn’t lead to lower salaries, reduced living conditions, and a persistently low “quit rate” among tech employees.

Technology is the great equalizer, and when it comes to employment, technology equalizes by reducing to the lowest common denominator rather than raising it.

Slowly, but surely (and then probably all of the sudden) Silicon Valley engineers will be replaced by their counterparts around the world.

Going “remote-first” is really just a euphemism for “offshoring,” which was itself really just a euphemism for, “outsourcing”, which was itself really just a euphemism for, “giving your job to someone in India because they’re just as good as you, work more hours, and cost 1/10th your salary without benefits.”

As I’ve written in the past, this is how the world works under a system whose design primarily incentives cost reductions to maximize shareholder value.

As US-based companies “go remote,” we need modern policies designed to protect American workers.

Enter UBI.

I am neither a proponent for UBI, nor am I adamantly against it. It is an unprecedented monetary experiment that has only just begun, and I’m not sure where it will lead. I do, however, believe that UBI is better fiscal & monetary policy than direct asset purchases. These asset purchases benefit the few at the expense of the many and only accelerate wealth inequality.

In a recent speech on Central Bank Digital Currencies (or CBDCs) at Consensus conference, ECB Executive Board Member, Yves Mersch concluded.

“the ECB respects technological neutrality. We do not serve technology — technology serves us.”

Wrong.

UBI is the result of deflation caused by technological innovation. CBDCs are the most efficient technology to deploy UBI.

So I’m sorry to break it to you Mr. Mersch, but you serve technology now.